Asset management has been one of the best-performing parts of the financial and related professional services ecosystem.

This first economic blog post of 2026 follows on from the last Economic Research report we published in 2025. For the first time in almost a decade, we undertook analysis on the global asset management sector and the UK's position within it. This post then builds on that research to look ahead at some challenges and opportunities the sector might face in 2026, as economic and political conditions remain volatile.

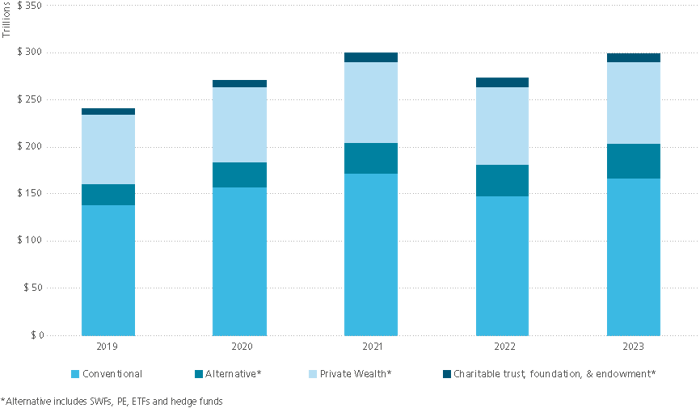

Our report sought to shine a light on the sector, which can often feel like an unsung hero within the wider financial services sector, often operating with less publicity than (for example) banking or insurance. However, asset management has been one of the best-performing sectors within financial services. Globally, we estimate assets under management (AUM) by the sector to have reached almost $3trn in 2023 – although this figure is indicative, not precise, since data and definitions are not directly comparable across sources.

Beneath that headline number sits an interesting diversification story. Conventional funds (pension, insurance and mutual funds) still account for the largest share of global AUM, at around two thirds of the total, but assets of alternative (non-conventional) funds have demonstrated growth that has been both fast (from a much lower base) and steady. In particular, hedge funds’ AUM totalled a record $5.1trn at the end of 2023, up by 168% from a decade earlier. Private equity AUM also reached a record in 2023, at just over $8trn.

Global asset management industry by type, 2019-2023

Source: TheCityUK calculation based on Thinking Ahead Institute, Investment company institute, International Association of Insurance Supervisors, McKinsey, ETFGI, BarclayHedge, Capgemini data

Within this global landscape, the UK has consolidated its role as one of the world’s leading hubs for asset management. In 2024, AUM by The Investment Association (IA) members increased by 10% year on year to £10trn. For the first time, more than half (51%) of all UK‑managed assets were sourced from overseas clients, underscoring the international orientation of the UK‑based sector. The UK’s position in Europe is particularly striking. The report shows that over one third (around 35%) of all European AUM is managed in the UK, placing it comfortably ahead of other major centres such as France and Switzerland.

One notable trend is the sustained growth in retail client assets as more individuals invest through funds and wealth managers. Retail client AUM saw almost 20% year-on-year growth in 2024. Institutional clients are by far the largest client segment; within that grouping, pension funds have traditionally been the largest single client type. However, the Investment Association notes that for the first time, “Retail investors became the largest client group in 2024, accounting for 28% of AUM. This highlights the increasing regulatory and policy focus on retail investors.”[1]

UK-managed equities by region (2014-2024)

Source: The Investment Association

This shift reinforces the case for two complementary measures: a cross-departmental national retail investment vision to align tax policy, regulation and financial education, alongside an individual investment scorecard to support a coherent framework for action. As set out in another of our recent reports, From cash to confidence: Building an investing nation, such an approach would ensure the UK’s ambitions are clearly articulated and joined up, while establishing consistent metrics to allow policymakers to track progress and assess the effectiveness of policy and regulatory reforms over time.

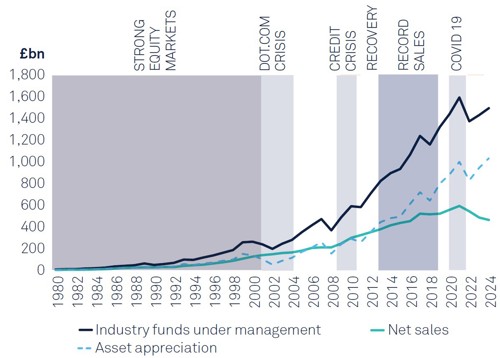

Looking ahead, it is clear that one of the main metrics of success carries with it an implicit vulnerability as well. Much of the recent rise in AUM has been due to favourable market movements rather than organic growth. Considering UK-based AUM, for example, the IA notes that “Since 2012, asset appreciation has consistently been the largest contributor to FUM growth”[2]

Drives of industry growth (1980-2024)

Source: The Investment Association

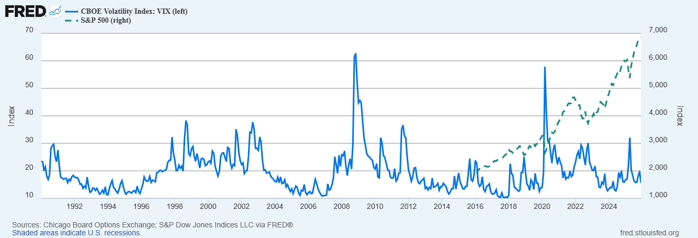

This underlines the sensitivity of the sector to asset-price cycles - a dynamic that is particularly important in an environment of elevated valuations and higher volatility. The chart below shows that we are in precisely this sort of environment at the moment. The blue line represents the benchmark measure of expected future stock market volatility[3], and the dashed line shows the value of the S&P 500 index:

Source: Federal Reserve Economic Data (Federal Reserve Bank of St Louis)

Note: monthly, data ending December 2025.

So, one important challenge for the asset management sector is ensuring it is well-positioned for any further bouts of market volatility, including a major market correction. Indeed, there are already reports of fund managers positioning themselves for an imminent correction, as described recently by the Financial Times[4] (among others).

Meanwhile, adoption of AI has the potential to enhance the sector’s performance not only through the much-discussed possibility of productivity increases, but also by helping to manage the sort of risk posed by the current environment. For example, machine learning models can analyse extremely large stock market datasets, identifying patterns and potentially finding early warning signals that may precede periods of heightened volatility. They can also simulate a wide range of market scenarios, facilitating stress-testing exercises and potentially helping firms anticipate potential drawdowns and adjust portfolio exposures proactively.

In conclusion, the asset management sector goes into 2026 with strong growth and a bigger global role, especially for the UK. More retail investors are joining, and both traditional and new types of assets are growing steadily. However, increasingly volatile economic and market conditions mean that the ability of firms to manage drawdowns and maintain client confidence may become even important for the sector’s stability and longer-term growth.

[1] The Investment Association, https://www.theia.org/sites/default/files/2025-10/Investment%20Management%20in%20the%20UK%202024-2025_1.pdf

[2] Ibid.

[3] The VIX Index, formally the Cboe Volatility Index, measures expected future volatility of the S&P 500 as implied by option prices. According to CBOE, “Volatility measures the frequency and magnitude of price movements, both up and down, that a financial instrument experiences over a certain period of time. The more dramatic the price swings in that instrument, the higher the level of volatility.” For more detail, see https://www.cboe.com/tradable-products/vix/#overview. VIX is often used as a proxy for generalised financial market volatility, although technically it captures only volatility of one particular US equity market index. That approach is reasonable, given that the S&P 500 accounts for around half of total global equity market capitalisation; for detail on the index, see https://www.spglobal.com/spdji/en/documents/additional-material/sp-500-brochure.pdf

[4] ‘Fund managers prepare for ‘reckoning’ in US tech sector’, 6 January 2026, available at: https://www.ft.com/content/48d9c100-0ec6-4edf-9395-eb44879ea5c6