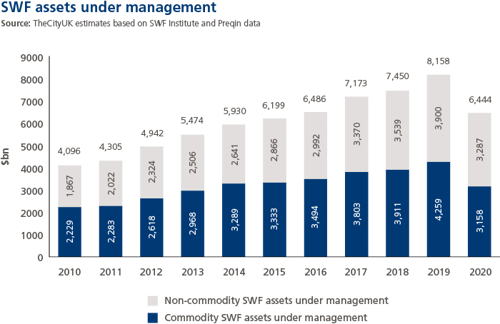

This economic research examines a financial services sub-sector that is often surrounded by a certain mystique: sovereign wealth funds (SWFs). The full report, ‘The UK as a leading centre for international sovereign wealth funds’, sheds light on a particular class of fund renowned for its relative lack of disclosure of data, examining the scale and segmentation of SWF assets under management and considering SWFs as critical providers of global capital.

The UK is one of the largest and most open markets in the world for fund management. London, as well as other cities such as Aberdeen, Birmingham, Cardiff, Edinburgh, Glasgow, Liverpool and Manchester, are important fund management centres.

London in particular is an important centre for SWFs as a clearing house and location from which some of these funds are managed. In addition, the UK’s role as a key destination for inward foreign investment and SWFs’ role as providers of global capital means that the potential for stronger and deeper partnerships between the UK and SWFs is significant.

At this time of economic and geopolitical upheaval, there is renewed debate about the UK’s competitiveness as a global financial services centre. But as SWFs continue to open international offices, the potential for the UK to continue its leading role as a host to some of the world’s largest and most important international investors remains undiminished.

Advantages of the UK as a centre for fund management

• A strong and responsive regulatory environment that is effective, fair and focused on the future.

• A demonstrated commitment by the government to the sector.

• A vibrant and supportive sector cluster in asset management and related professional services; the UK remains one of

the leading locations for asset management and is the top jurisdiction in Europe for funds under management, enjoying

sustained growth.

• A deep talent pool that supports all aspects of the asset management value chain.

• A strategic geographical location.

• State-of-the-art support services in front, middle and back office across the regional centres allowing cost efficiencies and

access to a diverse talent pool.

• An innovative ecosystem that promotes innovation and product development, e.g. Islamic Finance, renminbi trading, etc.