Geographical shifts in foreign direct investment have been modest—but noticeable.

Our Economic Research has often emphasised the important contribution financial services makes to the UK’s foreign investment position. For example, in our latest‘Key Facts’ report, we noted that financial services was the UK’s 2nd-largest sector in terms of inward FDI flows (cumulatively over 2020-23).

Cumulative inward FDI flow by top sector, £bn, 2020-2023*

Source: Office for National Statistics

*2019 data is classed as ‘confidential’

Note: A negative sign indicates a net disinvestment in the UK which means that direct investment interests were sold, and/or reinvested earnings were negative

FDI flows reflect the distribution of global capital; as such, they are related to countries’ economic weight in the world. In this blog post, I explore how global FDI patterns have evolved over the past decade. We have used IMF data[1] to examine whether the distribution of the stock of FDI[2] has kept pace with broader changes in global economic weight. Our initial, indicative analysis compared FDI stock in key country groupings—Advanced Economies, Emerging Markets and Developing Economies—between 2009 and 2023.[3] Our main findings are:

- the vast majority of the world’s FDI stock—which totalled $4trn in 2023—is in Advanced Economies

- that FDI was sourced, in the main, from other Advanced Economies, and

- this dynamic changed only marginally between 2009 and 2023.

FDI flows among Advanced/Emerging/Developing economies

Source: TheCityUK calculations based on IMF data

2009 left-hand side, 2023 right hand-side

Note: visualisation represents Outward Direct Investment liabilities (gross), debt instruments, all entities.

The most noticeable change is the weight of Emerging Markets (represented in the charts above in green) in global FDI. In 2009, Emerging Markets were the source of only 2% of the global stock of FDI; by 2023 this had increased to 6%. This was because of a 10-fold increase in dollar terms, from $22bn in 2009 to $225bn in 2023.

It is important to emphasise that this analysis is indicative. The data presented here reflect official data reported by countries to the IMF—but participation is voluntary. In particular, the negligible values for Developing Economies are likely to reflect a lack of data, or a lack of reporting.

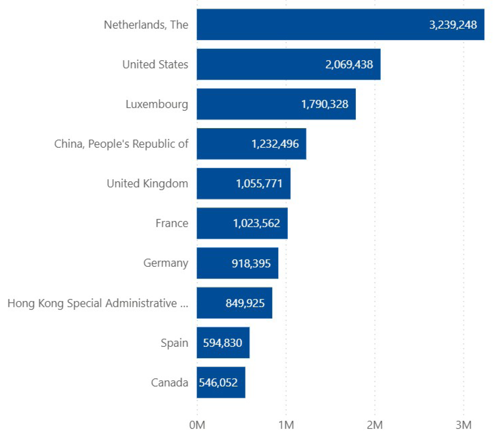

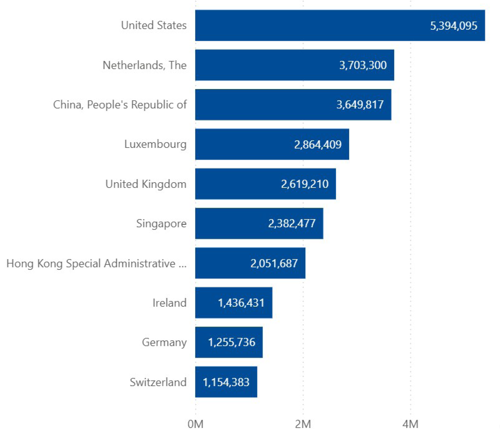

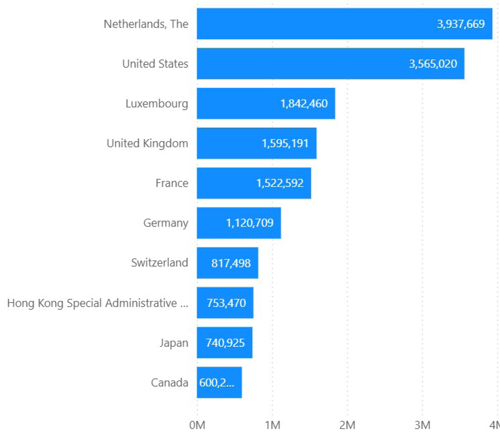

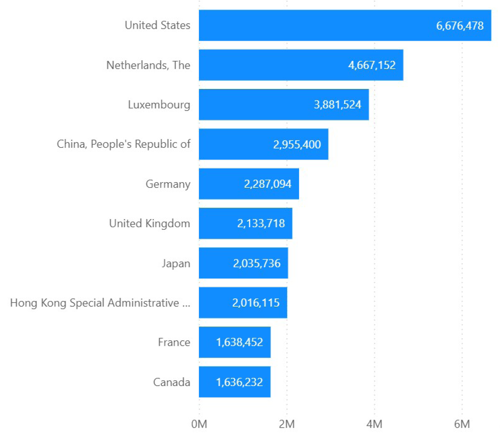

China, with its unparalleled economic growth and concurrent reshaping of global manufacturing and investment structures, is a significant part of the Emerging Markets story. The charts below show that in 2023, China was the world’s fourth-largest source of FDI.