Read the speech given by Anjalika Bardalai at TheCityUK Annual Conference 2022.

Good morning everyone. I’m delighted to be able to share with you highlights of the research we’ve launched today – our flagship report, ‘Key Facts about UK-based financial and related professional services’. This is an annual statistical guide to the many ways in which the UK-based financial and related professional services industry makes a direct and indirect contribution to the economy.

I don’t believe the old saying that familiarity breeds contempt, but this report is the one that’s perhaps most closely identified with TheCityUK and it’s the source of some of our best-loved statistics – including some that you’ve already heard this morning. But because some of the content is very familiar, I want to start with a reminder of why the findings of this report are important.

These are examples of news headlines from just the past week. Public debate is dominated by issues of low growth and high and rising inflation, so I won’t dwell on the macro outlook. But it’s worth looking at this in just a bit of detail before we come on to the role of our industry in improving things.

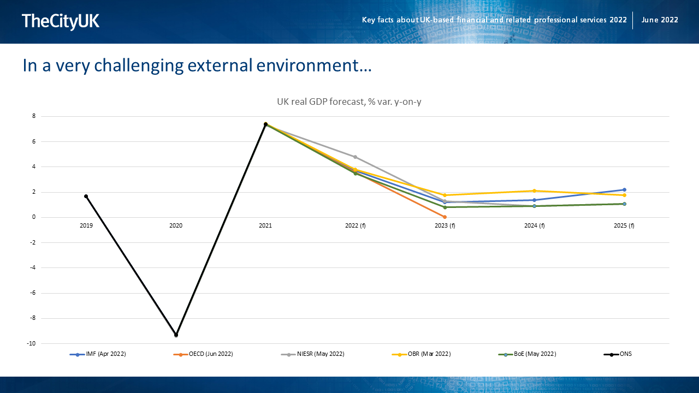

This chart shows the expectations of official forecasters for UK GDP growth over the next three years.

You can see that after the 7% growth registered last year which followed the 9% contraction in 2020, growth is again expected to slow quite significantly this year, to around 4%. But then, worryingly, it’s expected to almost grind to a halt in the subsequent three years. I think there two key points to emphasise.

First, unfortunately the idea of a post-Covid economic boom now looks like very wishful thinking indeed. Second, that uncertainly is happily less than it was a year or two ago, but alas risks to the outlook remain very high, and they’re almost exclusively on the downside. The IMF’s latest WEO lists no fewer than eight separate downside risks to the global outlook ranging from debt distress to a worsening of the geopolitical environment – and also notes that many of these risks are interconnected.

But what does all this have to do with FRPS and our discussions today?

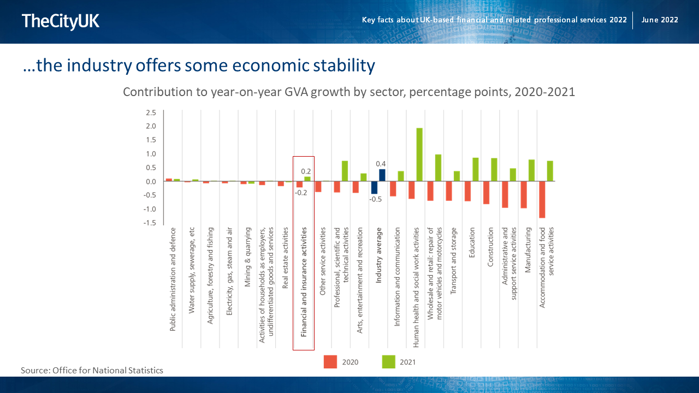

This chart shows you that the industry has exhibited relative stability throughout the pandemic period.

These are not growth rates – these are the contributions to overall GVA growth that different sectors made, and you can see that financial services in particular experienced much less of a swing in the contraction of 2020 and then the recovery of 2021 than other industries did. In that sense, you could say that the industry served a function a bit like ballast in stabilising a ship.

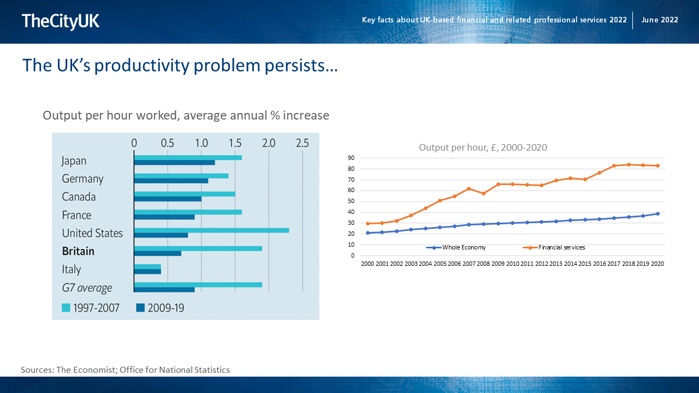

Meanwhile, one of the biggest structural challenges facing the UK is the low rate of productivity growth. We’d need a whole session just on productivity to do justice to the topic, but briefly, here you can see that productivity growth has fallen across the G7 since the 2008-09 financial crisis, but the fall has been particularly steep in the UK.

However, there are a few bright spots amidst the gloom of UK productivity data – and one of them is financial and related professional services. On the right you can see that productivity in financial services has consistently been above that of the economy as a whole. And although the industry’s productivity growth has been weaker in recent years than it was before the financial crisis, overall over the past two decades its productivity growth rate has been almost double that of the whole economy, at 5.5% compared to 3.1%.

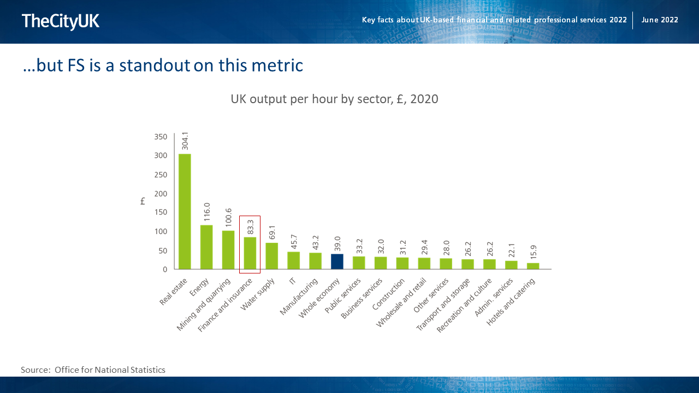

And here you can see that in 2020, which is the latest year for which full-year data are available, Financial services was the UK’s fourth most productive sector.

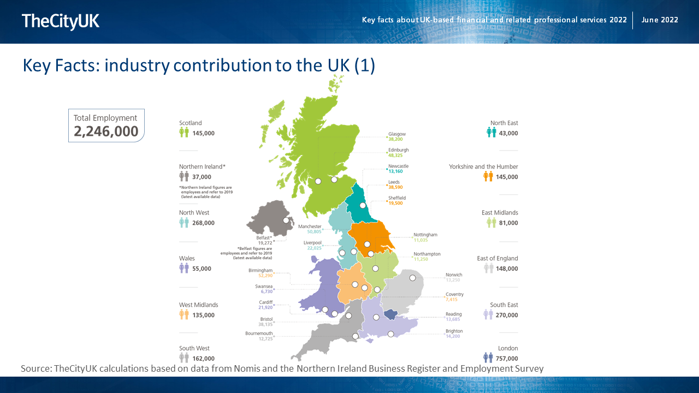

These points are all in our new research. But also, obviously I can’t go through this presentation without sharing some of those very familiar data points that we all know and love. This graphic shows you the spread of FRPS employment across the UK – and I want to flag that we’re currently working on our annual research exploring the contribution of the industry to regional economies, and we’ll be publishing that in September, so I do hope to see many of you again then when we launch that.

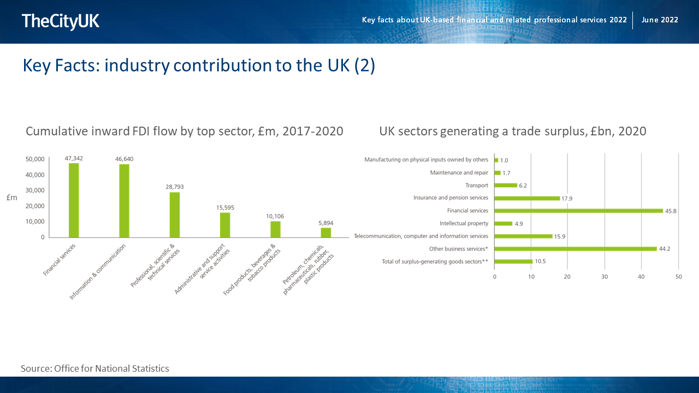

Another aspect of the industry’s direct economic contribution is through the external sector: trade and investment.

Here on the left you see that over the last 4 years, which is as much data as was available, financial services was the largest recipient of FDI, and the wider professional services category that includes our RPS of legal, accounting and consulting was also a significant recipient.

The chart on the right is about trade - you see all the sectors that individually run trade surpluses. All of them are service sectors, except the last bar which is where we’ve combined the values for all goods sectors that generate a surplus. And you can see that financial services runs the largest surplus by far. And again, the ONS includes what we call related professional services in a wider category of ‘Other business services’. But you can see that wider category runs the second-largest surplus. This means that overall, the financial and related professional services industry plays a crucial role in partially offsetting the deficits generated by other sectors and thus helping to stabilise the balance-of-payments position.

And I’d add that in an environment where sterling is depreciating and slowing global growth may put pressure on UK exports, that stabilisation factor becomes all the more important in helping to mitigate pressure on the current account.

I haven’t yet mentioned the biggest macroeconomic indicator of all, which is GVA. I don’t want this to be death by numbers so suffice to say that financial and related professional services is one of the UK’s largest industries in terms of economic contribution.

And coming back to the point I made earlier about how its contribution was relatively stable throughout the wild economic swings we’ve seen in the past couple of years – it’s because a lot of the products and services it provides are fairly fundamental. Of course some are discretionary, but the ecosystem really provides a foundation that allows the rest of the economy to function.

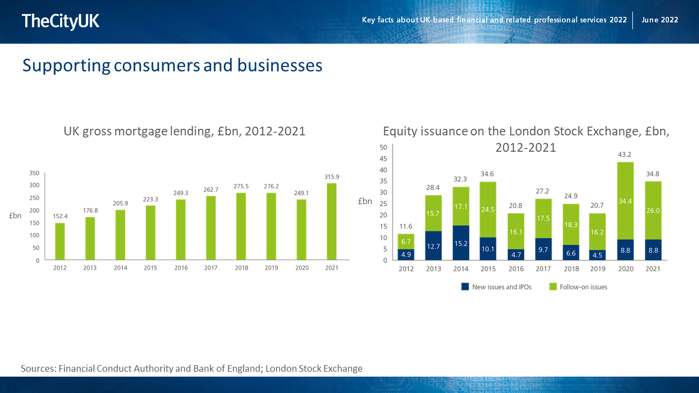

So in my penultimate slide I wanted to share a couple of examples from our research about the industry’s role as a facilitator.

Here you see mortgage lending, which had grown steadily until the onset of the pandemic and then recovered last year after the fall in 2020.

You also see equity issuance values, one of the key ways in which companies raise funds.

So in a short: a snapshot of the way the industry directly helps businesses and consumers.

I hope you’ll look at the full report to get a sense of some of the other indicators. But before I wrap up, I wanted to go back to the question about why all this is important. And I’ll leave you with two points that I think start to answer that question.

First: the industry is important because it plays a stabilising and enabling role in the economy, which is always fundamentally important but perhaps even more so at a time of increasing economic distress.

Second: this research is important because it provides specific examples and metrics of the value of an industry that is still too often either misunderstood or maligned. And of course an important part of that is quantifying the value, because it makes clear the huge scale of the offering. But I think it’s also important to recognise that the qualitative message is as important as the big numbers – in part because not all of the value of the industry can be quantified.

So to conclude I want to leave you with one economist’s summary of what a financial system provides

Robert Merton is a joint Nobel Prize winner with Myron Scholes – famous for the Black-Scholes model.

This is from a paper he published almost 30 years ago but I wanted to use it to close my remarks because it offers a way to consider the facts in our report from a wider perspective. So many aspects of financial and professional services are so embedded in our lives that at this point we take them for granted, so it’s worth going back to first principles and considering what is it we’re actually getting when we have a robust financial services system.

Think about pooling funds, where an example of the principle is syndicated loans. A very current example I can give you, drawing on the economic research we published just a couple of months ago, is that almost all green and sustainable lending (not debt financing more widely, just lending), which is critical to the government’s net-zero target, is done through syndicated loans – partly because some of the projects being funded are extremely large, and partly because in some cases the risk is perceived to be higher.

So hopefully that’s given you some food for thought as well as some key statistics. And with that, let me invite you to look at our new research in more detail.