Our final economic research report of this year, the 2018 edition of our annual ‘International Key Facts’ report, once again set out the UK’s position as the leading global financial and related professional services centre. Although the research presents a wide range of data, it’s inevitably the trade statistics that are most often discussed.

This year, our research found that the UK’s financial services trade surplus was more than £60bn. (The trade surplus data in our recent report were sourced from UNCTAD, to facilitate international comparisons; the trade surplus figure is slightly different from that reported by the Office for National Statistics (ONS). But this post makes use of ONS data. The trade surplus comprises £78bn worth of industry exports and £17bn of imports, according to ONS data.)

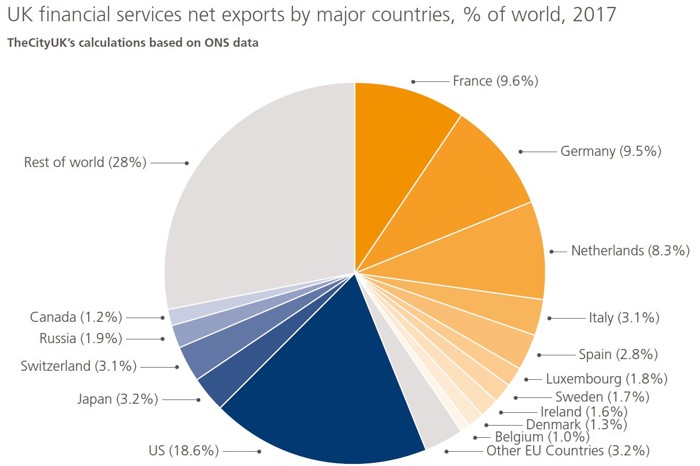

Our report showed that the EU and the US account for the vast majority of the industry trade surplus:

But because the UK’s financial services imports are so small, looking at the exports alone would present a similar picture. (The chart above shows net exports, which is the trade balance, or exports minus imports.) In fact, just three countries accounted for 50% of all UK financial services imports: the US (which exported £5bn worth of financial services to the UK), Japan (£2.1bn) and Germany (£1.6bn). UK financial services trade is quite geographically concentrated—a point I’ve raised in previous posts.

The annual data presented in the ONS’s Pink Book are a useful snapshot, but more timely data can provide a more detailed picture. Until last month, however, the quarterly data on the UK’s trade in services didn’t allow us to look at financial services because they were based on the International Trade in Services survey—and this survey excluded the category ‘banking and other financial institutions’ (along with other important services sectors like travel, transport and higher education, among others).

But the most recent quarterly data, covering April-June 2018, represent a major improvement. For the first time, the statistics cover the UK’s entire services economy, captured in 31 different sectors. These data show that financial services trade surplus reached £16.6bn in Q2 2018, up by 5.7% from the previous quarter. Financial services exports contributed 29.4% of total services exports in that quarter.

The new data have been published as part of the ONS’s broader trade development plan, which has evolved because “the demand for improved and more detailed UK trade statistics has increased significantly since the EU referendum.”[1] Encouragingly, even more developments are in the pipeline, including further analysis on trade asymmetries (which I have written about here) and additional detail on modes of supply of services.

This latter area is of particular interest given the extent to which it is likely to affect how services trade is recorded. “Modes” refers to the World Trade Organisation’s (WTO’s) Modes of Supply, which describe four different types of trade in services. These are summarised here:

This simple summary most likely goes quite a long way towards explaining why services features to such a limited extent in the collective consciousness of trade—because services trade is much less easy to picture than the idea of selling food products into overseas markets, for example, or buying a luxury garment imported from another country.

The table also helps explain why services trade is so difficult to measure. The WTO is clear that its Modes of Supply for services are “significantly broader than the balance of payments concept of services trade.”[2] In other words, some activity within the four modes would certainly be classified as trade in the balance-of-payments (BOP) framework—but other activity would be classified as income, which is another component of the BOP.

For example, imagine a UK bank established a local presence in Country X to serve customers in Country X. If the local operation remained a UK entity (e.g., a branch or representative office of a UK group), its revenue in Country X would be considered a UK financial service export. If, however, it became resident of Country X (as, say, a locally incorporated subsidiary), then its revenue there would be considered investment income. This means that what is captured in a country’s trade statistics (the UK’s £78bn of financial services exports, for example) almost certainly excludes some activity that would be captured under GATS Mode 3. But such activity isn’t unrecorded—it just shows up elsewhere in the BOP.

How much does this matter? Services trade is still a fraction of goods trade—in the UK, for example, services exports and imports totalled £443bn in 2017, compared with total merchandise trade of £815bn (although the real picture is almost certainly more nuanced, given the difficulty of accurately capturing the services elements embedded in various goods). But a more detailed understanding of how the aggregates break down—both in terms of types of transactions, types of business (e.g. wholesale or retail), and sub-sectors within broader categories like “financial services”, would enhance economists’ and policymakers’ understanding of this complex but increasingly important part of the global economy.

[1] Office for National Statistics, ‘UK trade statistics transformation: achievements and forward look, October 2018’

[2] https://www.wto.org/english/tratop_e/serv_e/cbt_course_e/c1s3p1_e.htm