Always important, better financial literacy will be crucial as economic and financial difficulties mount.

I recently had the pleasure of speaking at the Annual Conference of FairLife, a charity promoting financial education and fair trading in financial services. Financial education—and financial literacy in particular—is a long-standing issue in the UK, and I have written in the past about its importance (for example, noting that OECD research has found the level of financial literacy in the UK to be below that of the country’s peers).

The financial services sector is sometimes criticised for offering products that are confusing. It certainly has a responsibility to offer appropriately-designed products and services which are explained in clear, jargon-free language. But consumers, too, have a responsibility to equip themselves with basic arithmetic skills and an understanding of concepts like percentages and probability in order to properly assess the products and services they are offered, and evaluate the risks and benefits of each. Improving financial education for children will be crucial for equipping the consumers of tomorrow, but it is clear that financial literacy among today’s adults is not as high as it needs to be. Startlingly, it was revealed at FairLife’s conference that a survey conducted by a major retail bank indicated that more than one-quarter of the bank’s credit-card customers thought that the higher the APR, the better for them.

Inadequate levels of financial literacy are a roadblock preventing true financial inclusion, and a barrier to ensuring that the financial services sector benefits all levels of society. And this is a particular problem at a time when consumers are facing the prospect of much higher levels of financial risk and economic insecurity thanks to the combination of slowing growth, rising inflation and a highly uncertain policy and macroeconomic environment.

Consumers in all parts of the country have become much more vulnerable. For example, research by the Centre for Cities demonstrated the impact that high inflation is having on real wages in cities across the UK:

Source: Centre for Cities

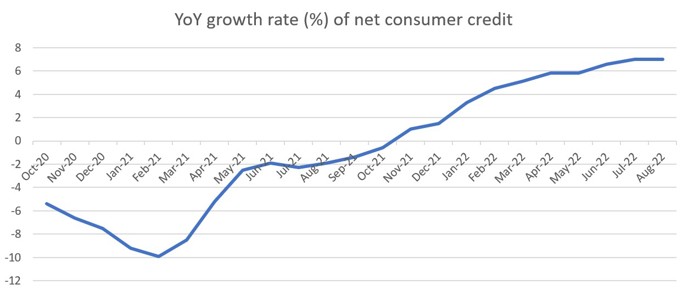

Households are increasingly turning to credit. After turning negative during the acute phase of the pandemic (April 2020-October 2021), consumer credit growth has risen steadily over the past year and averaged 7% year on year in the latest three months (June-August), according to data from the Bank of England.

Source: Bank of England

Note: data are seasonally adjusted and exclude student loans

Credit card spending was a key driver of overall credit uptake, and data from UK Finance shows that between December 2021 and June 2022 (the latest available data), spending on travel was the main driver of growth in credit-card spending.[1] Since this period includes the Easter and summer holiday seasons, this is not entirely unsurprising, although it does reflect a strong degree of pent-up demand as well as—perhaps—some degree of consumer confidence in that period.

However, the tide has turned since the summer. GfK’s flagship consumer confidence index has declined steadily in recent months, and September’s reading of -49 was a record low.[2] According to a recent survey conducted by the Office for National Statistics covering the early part of September[3]:

- 29% of adults reported that they found it very difficult or difficult to pay their usual household bills in the last month compared with a year ago.

- 18% stated that they had to use savings to cover living costs.

- 12% stated that they had to borrow money or use credit.

These figures are worrying. In the months ahead more households will use credit to meet basic needs rather than to fund discretionary purchases like holidays. At the same time, the Bank of England has signalled that it will continue to tighten monetary policy, so that some households are likely to face higher debt-service costs on higher amounts of outstanding debt. In the context of average wage growth not keeping pace with inflation for essentials like food and energy, plus the prospect of higher unemployment—the Bank of England forecasts unemployment to rise to 4.4% next year, 5.5% in 2024 and 6.3% in 2025[4]—this is a potentially explosive combination that could have significant consequences for both borrowers and lenders (given the likelihood of increased risk of defaults).

It is a reminder that although many things will remain outside of individuals’ control in these turbulent economic times, individuals and institutions should at least capitalise on existing partnerships and engagement platforms to try to create a society that is as well-informed as possible. At this institutional level, it is not only financial and related professional services firms (lenders as well as professional advisers) who are involved; charities and education providers (both traditional and digital) have a role to play working in partnership with the industry to try to improve societal outcomes.

[1] UK Finance, Household Finance Review – Q2 2022

[2] https://www.gfk.com/en-gb/press/uk-consumer-confidence-tumbles-to-new-low-of-49-in-september

[3] Office for National Statistics, Public opinions and social trends, Great Britain: 31 August to 11 September 2022, available at: https://www.ons.gov.uk/peoplepopulationandcommunity/wellbeing/bulletins/publicopinionsandsocialtrendsgreatbritain/31augustto11september2022

[4] Bank of England, Monetary Policy Report August 2022, available at: https://www.bankofengland.co.uk/-/media/boe/files/monetary-policy-report/2022/august/monetary-policy-report-august-2022.pdf?la=en&hash=0F0E2DC12F8C853F2D604B75B620D03FD58BC07D