2023 was a better year than expected, but the outlook for the year ahead is highly uncertain.

Towards the end of last year, I had the opportunity to travel to Liverpool at the invitation of the Department for Business and Trade, to present our economic research at an event as part of their International Trade Week. The research in question was our new report analysing financial and related professional services exports from the various British regions and nations. But I was able to set the research findings in the wider macroeconomic context.

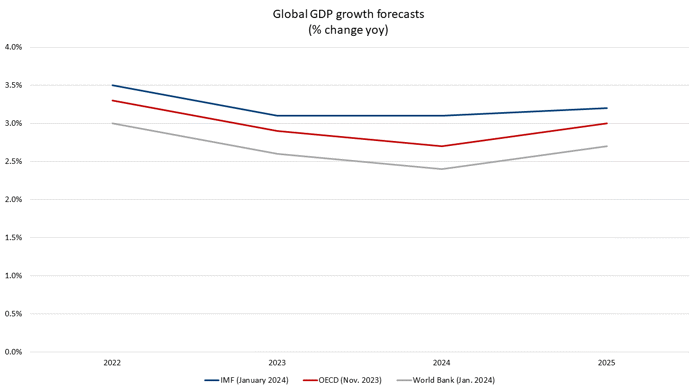

Part of that context-setting was discussing the expectations for global economic growth in 2024. Official forecasters do not expect a recovery until 2025—and even then, they anticipate it will be a modest one:

Many economy-watchers were surprised by the resilience of Developed Markets in 2023. For example, in its latest (January 2024) forecast, the World Bank revised up its estimate for global growth in 2023 to 2.6%, from 2.1% in its June 2023 forecast. But the forecast for Emerging Market and Developing Economies in the aggregate was unchanged, whereas the forecast for Advanced Economies was revised up by almost a full percentage point between June 2023 and this month. The US was the main driver of this stronger outlook.

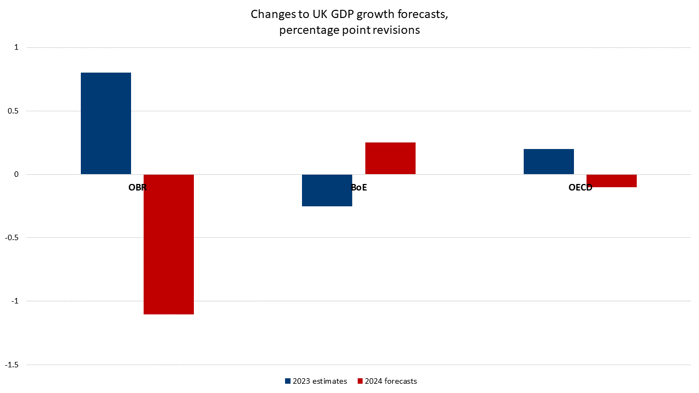

The outturn for UK GDP growth in 2023 is now generally estimated to be higher than initially expected, and UK forecasts have gradually been revised up over the course of the year. However, forecasts for 2024 have been revised down, indicating that some of the economic pessimism has merely been brought forward. Put another way, it is perhaps not the substance of forecasters’ concerns about the UK outlook that were misplaced, but just the timing of when those concerns would materialise. The Bank of England is an exception in this regard, having revised down its growth estimate for 2023 but raised its forecast for 2024.

The chart below shows this graphically, presenting the percentage point revisions to GDP growth estimates/forecasts for 2023 and 2024 of the Office for Budget Responsibility, Bank of England, and OECD.

Source: TheCityUK calculations based on OBR, BoE and OECD data.

Note: The OBR forecasts were published in March and November 2023; the BoE forecasts were published in November 2023 and February 2024; the OECD forecasts were published in September and November 2023.

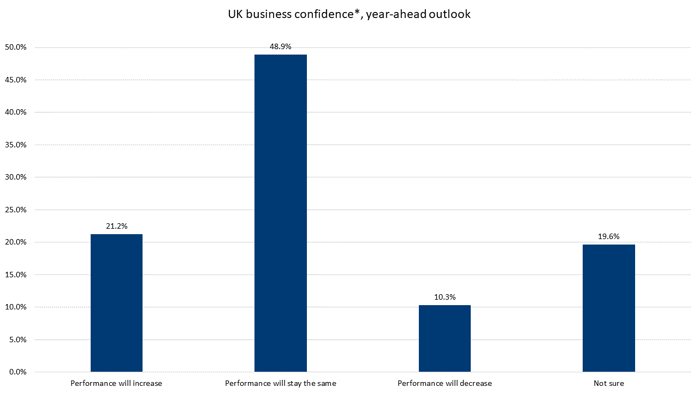

Despite these lacklustre growth prospects, UK businesses remain sanguine. The latest data from the Office for National Statistics’ BICS survey shows businesses feeling relatively confident about prospects in 2024:

*Question: How do you expect your business’s overall performance to change over the next 12 months? (Release date: 14 December 2023- Period: November 27th to December 10th )

Source: ONS BICS

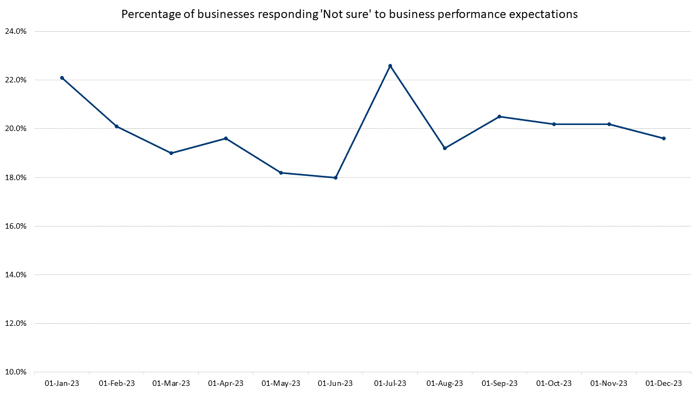

But something worth noting—as I’d highlighted when presenting this data in Liverpool—is that around 1 in 5 businesses responded to the question ‘How do you expect your business’s overall performance to change over the next 12 months?’ by saying, in effect, ‘we don’t know’. Moreover, that uncertainty has been persistent—the percentage of businesses responding ‘not sure’ has hovered at around 20% for the past year:

Source: ONS BICS

Source: ONS BICS

This sense of uncertainty is also apparent among the UK’s finance chiefs, as reflected in the latest edition of the long-running CFO Survey undertaken by Deloitte. As Deloitte’s Chief Economist, Ian Stewart, summarised it: “CFOs start 2024 in a positive mood, but one tempered by high levels of uncertainty”.[1] Deloitte’s data show that 50% of respondents rated the level of external financial and economic uncertainty facing their business as high or very high in Q4 2023, up from 46% in Q3 but down from 61% in Q4 2022. The low base of comparison for the improvement in sentiment goes some way to explaining the survey’s finding that “Defensive strategies such as cost reduction, increasing cash flow and reducing leverage remain the top priorities for CFOs”[2], notwithstanding an overall improvement in CFO sentiment.

As the latest official data showed a marked decline in retail sales volumes in the crucial December trading month[3], as well as a surprise increase in consumer price inflation in December compared with November (albeit only a one-tenth-of-a-percentage-point rise), the caution among business leaders as well as economic forecasters appears to be warranted.

[1] Deloitte, ‘The Monday Briefing’, 8 January 2024, available at: https://blogs.deloitte.co.uk/mondaybriefing/2024/01/a-positive-start-to-2024.html

[2] Deloitte, ‘CFO Survey Q4 2023’, available at: https://www2.deloitte.com/uk/en/pages/finance/articles/deloitte-cfo-survey.html

[3] ONS, https://www.ons.gov.uk/businessindustryandtrade/retailindustry/bulletins/retailsales/december2023