Understanding the dynamics of headline-grabbing developments in the labour market requires sector-specific analysis.

In the speech I gave recently to launch the 2022 edition of our ‘Key Facts about UK-based financial and related professional services’ report, I’d emphasised how timely the research was given the backdrop of slow economic growth and high and rising inflation.

Since then, these issues have moved even more to the fore as the macroeconomic picture has darkened considerably. Data released yesterday showed that consumer prices increased by 10.1% in the year to July, up from 9.4% the previous month. In its headline-grabbing Monetary Policy report published on 4th August, the Bank of England forecast that after moving into recession in late 2022 the UK economy would contract by 1.5% in 2023 and a further 0.25% in 2024. This is far more pessimistic than the forecasts of either the IMF or the OECD, with their 2023 growth projections of 0.5%[1] and 0%[2] respectively.

Meanwhile, earlier this week the Office for National Statistics (ONS) published data showing that real wages declined by 3% year on year in April-June. Real wage growth matters enormously not only because of its implications for the well-being of individuals and households, but also because the UK economy relies heavily on consumer spending. The Bank’s Monetary Policy Committee “continues to assume that some households absorb part of the fall in their real incomes by saving less of their current income or by spending some of their stock of savings. Consistent with this, a quarter of respondents to a recent ONS survey, who are facing a rise in the cost of living, expect to use their savings to support their consumption.”[3]

In my next blog post I will delve into the savings draw-down issue. For now, it’s worth looking in more detail at labour market data—especially since with its recent monetary tightening, the Bank is trying to tackle the risk of medium-term, second-round inflationary effects rather than the near-term inflation driven by high energy prices (by its estimate, energy costs are contributing at least 80% of overall price rises if both indirect and direct effects are considered).

The ONS data shows that the mean of year-on-year growth in average weekly earnings was 6% over January to June 2022, although the ONS notes that there is a slight skew to this figure given that “Bonus payments are continuing at the high levels seen over the last six months, after a slightly lower level in May 2022.”[4]

However, wage increases are not evenly distributed throughout the labour market. For example, the gap between public and private sector wage inflation (January to June average) is significant, at 5.3 percentage points. Our economic research has previously highlighted the contribution the financial and related professional services industry makes to the UK economy in the form of highly-skilled, high-wage jobs (among other things). The latest ONS data show that the increase in average weekly earnings in the category ‘Finance and business services’ averaged 8.3% year on year in January-June, compared with 6% for the whole economy and 6.2% for services overall. This was on par with the wage increase in ‘Wholesaling, Retailing, Hotels & Restaurants’ (8.2%), although in the latest quarter wage rises in wholesale, retail and hospitality outpaced those of every other sector.

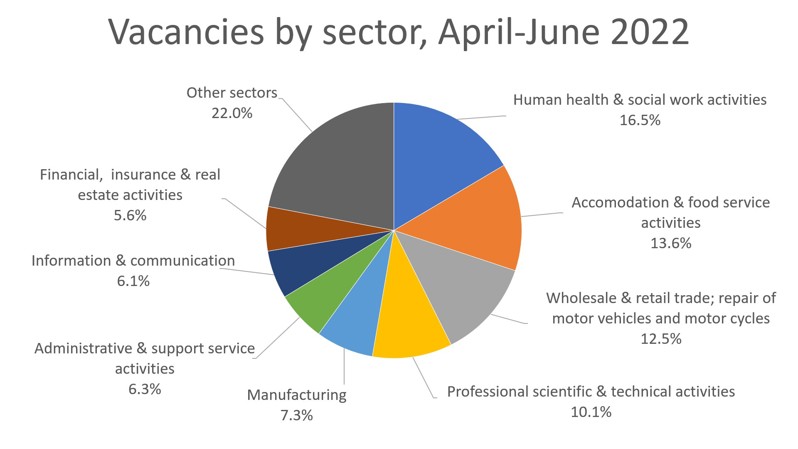

Conventional wisdom is that these rapid wage increases reflect a tight labour market. Press headlines talk giddily about how the labour market is de-coupled from fears of the looming recession.[5] But this overlooks the extent to which vacancies and hiring difficulties are concentrated in certain sectors. Of the 1.3m economy-wide vacancies recorded in April-June 2022, more than 40% were in just three sectors: health and social work; accommodation and food service; and wholesale and retail trade and motor repairs:

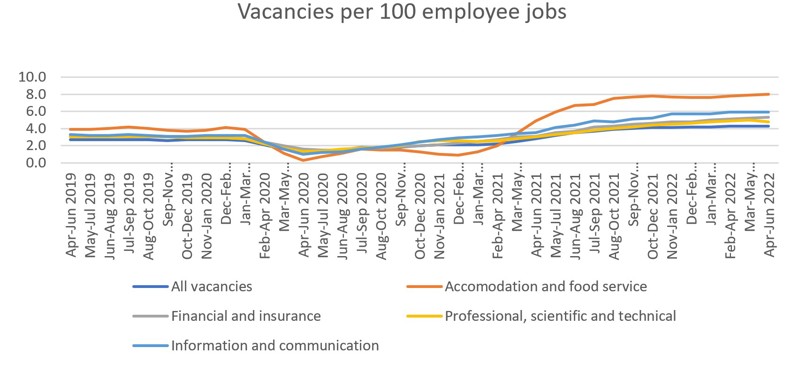

Looking at vacancies per 100 employee jobs, accommodation and food service is the only sector whose figure was very significantly higher than the economy-wide figure of 4.3, at 8. It is also useful to consider current vacancy levels relative to their pre-pandemic trends. Again, accommodation and food service stands out as the sector whose vacancy rate is significantly higher than its pre-pandemic trend. In financial services, there was an average of 5.2 vacancies per 100 employee jobs in January-June 2022, compared with an average of 3 in April 2019-March 2020. In professional, scientific and technical activities (the wider category that includes the related professional services of legal, accounting and management consulting), the January-June 2022 average was 4.9 compared to 3 before the onset of Covid-19.

So as we seek to understand the economy in these unusual and fast-changing conditions, we should bear in mind that headlines and narratives about labour shortages are overly simplistic. A better understanding of the economy—and, crucially, where it is headed—requires looking at sector-specific detail. There is always a danger in relying too heavily on averages, which by necessity mask underlying variation; but this danger is perhaps more acute in the context of labour markets, where workers are far from fungible!

[1] International Monetary Fund, World Economic Outlook: Gloomy and more uncertain, (July 2022), available at: https://www.imf.org/en/Publications/WEO/Issues/2022/07/26/world-economic-outlook-update-july-2022

[2] OECD, OECD Economic Outlook Volume 2022 Issue 1, (June 2022), available at: https://www.oecd-ilibrary.org/sites/62d0ca31-en/1/3/2/46/index.html?itemId=/content/publication/62d0ca31-en&_csp_=0cf9a35c204747c5f82f56787b31b42b&itemIGO=oecd&itemContentType=book

[3] Bank of England, Monetary Policy Report, 4th August 2022, p.17, available at: https://www.bankofengland.co.uk/-/media/boe/files/monetary-policy-report/2022/august/monetary-policy-report-august-2022.pdf

[4] Office for National Statistics, ‘Average weekly earnings in Great Britain: August 2022’, 16th August 2022, available at: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/averageweeklyearningsingreatbritain/august2022

[5] For example, ‘Record number of job adverts as labour market defies slump fears’, The Times, 12 August 2022, available at: https://www.thetimes.co.uk/article/e50e07f8-1990-11ed-b4a0-f11f082a3a3c?shareToken=4df6a04e9e6295ea0e33a31eadb8ba9a. But this is one of many examples.